How Do Interest Rate Hikes Impact Bitcoin Prices?

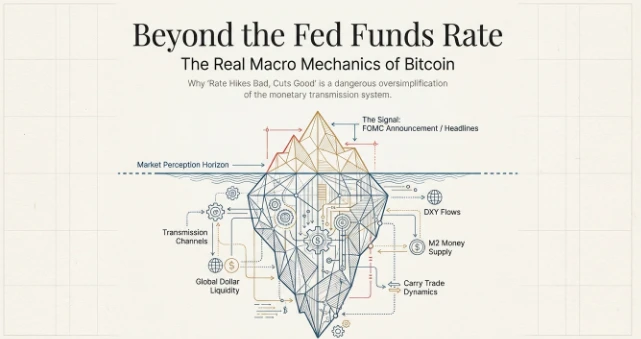

Interest rate hikes don’t kill Bitcoin directly — they drain the environment Bitcoin needs to thrive. Understanding exactly how that drainage works can help you stop making the same reactive mistakes most retail investors make around every Fed meeting.

Last Updated: February 2026 · 3,800-word deep dive · Educational purposes only

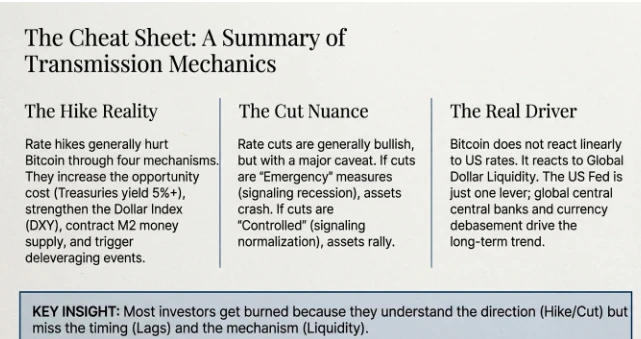

- When the Fed raises rates, risk-free assets (like Treasury bonds) suddenly yield 5%+ returns — making Bitcoin’s 0% yield look unattractive by comparison.

- Higher rates strengthen the U.S. Dollar (DXY rises), and since Bitcoin is priced in dollars globally, a stronger dollar makes Bitcoin more expensive and reduces demand.

- Rate hikes shrink M2 money supply — less dollars in the system means less speculative capital flowing into Bitcoin.

- Institutional investors using borrowed money (leverage) get margin calls and are forced to sell their most liquid assets, including Bitcoin.

- But the relationship isn’t always linear. Rate cuts sometimes cause Bitcoin to drop too — when they signal a recession, not just cheaper money.

Most articles will tell you “rate hikes are bad for Bitcoin” and leave it there. That’s the surface answer, and it’s also why most people get burned — because they understand the direction but not the timing, the mechanism, or when the rule breaks completely.

Let’s go deeper.

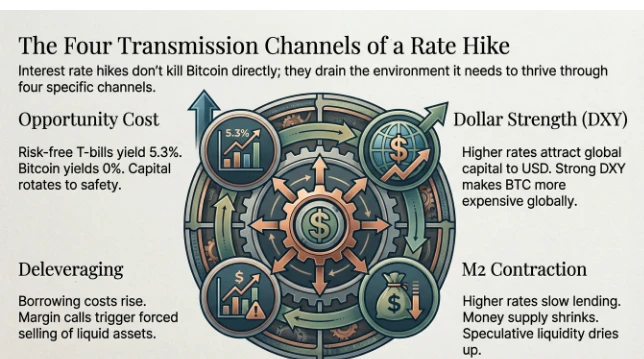

Why Do Interest Rate Hikes Make Bitcoin Drop? The Four Transmission Channels

There are four distinct ways a Fed rate hike puts downward pressure on Bitcoin. They don’t all happen at once, and they don’t all hit with equal force. But when all four activate simultaneously — like they did in 2022 — Bitcoin dropped from $48,000 to $16,000 in under twelve months.

Here are the four channels:

01

Opportunity Cost

When 3-month U.S. Treasury bills yield 5.3% with zero risk (as they did in mid-2023), holding Bitcoin — which yields nothing — costs you that 5.3% every year in foregone returns. Rational capital rotates out.

02

Dollar Strength (DXY)

Higher U.S. rates attract global capital into dollar-denominated assets. This strengthens the U.S. Dollar Index (DXY). Since Bitcoin trades globally in dollars, a stronger dollar makes Bitcoin more expensive for foreign buyers, reducing demand.

03

M2 Money Contraction

Higher rates slow bank lending and increase bond yields, pulling dollars out of circulation. M2 money supply — the broadest measure of available money — shrinks. Less dollars in the system means less speculative capital available to flow into Bitcoin.

04

Risk-Parity Deleveraging

Institutional funds using leverage (borrowed money) face higher borrowing costs. When their portfolios decline, brokers issue margin calls. Bitcoin, being the most liquid 24/7 market, gets sold first to raise cash. This cascades.

Understanding these four channels separately is important because they don’t all reverse cleanly when rates get cut. That’s the part nobody talks about.

The opportunity cost effect fades quickly when rates drop. But the M2 contraction takes 6–12 months to reverse. And the behavioral damage — retail investors who got burned and left the market — takes even longer to repair. This is why Bitcoin doesn’t bounce back overnight after a rate cut.

Common Mistake

Most people watch the Fed rate announcement and immediately trade Bitcoin. In reality, the market had already priced in the expected decision 2–4 weeks earlier through futures markets. The actual announcement day is often the wrong time to act — what matters is whether the decision surprised the market relative to expectations.

Is Bitcoin’s Correlation With Interest Rates Truly Negative? What the 2020–2025 Data Actually Shows

Here’s where things get counterintuitive — and where most articles mislead you with oversimplification.

The correlation between Bitcoin and the Federal Funds Rate is not consistent. Over short 30-day windows, the correlation coefficient fluctuates between -0.02 and -0.45, depending on what else is happening in the macro environment. Some periods show almost no relationship. Some periods show an extremely tight inverse relationship.

And here’s the finding that genuinely surprised researchers: when the European Central Bank (ECB) hiked rates in 2022-2023, Bitcoin prices in euros actually rose during portions of that cycle. Why? Because ECB hikes weakened the euro relative to the dollar, making dollar-priced Bitcoin cheaper for European buyers. This increased demand, partially offsetting downward pressure from the U.S. side.

The lesson: it’s not “rate hikes bad for Bitcoin” — it’s specifically Fed rate hikes that strengthen the U.S. dollar that pressure Bitcoin, because the entire global crypto market is dollar-denominated.

| Period | Event | BTC Price Change | Key Driver |

|---|---|---|---|

| Mar 2022 – Nov 2022 | Fed hikes 425bps (fastest in 40 years) | –67% | All 4 channels active simultaneously |

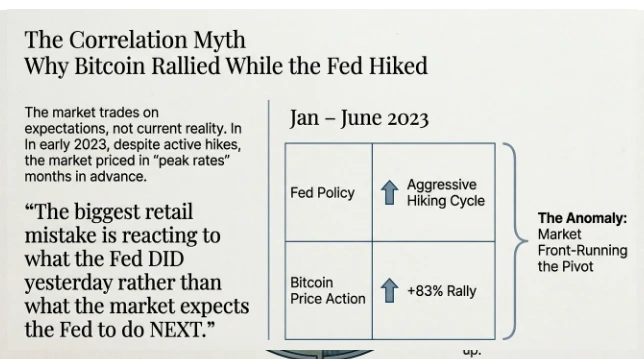

| Jan 2023 – Jun 2023 | Fed hikes continue, but pace slows | +83% | Market priced in “peak rates” early |

| Aug 2024 | Fed signals coming cuts; BoJ hikes | –26% (brief) | Japanese carry trade unwind |

| Sep 2024 | Fed cuts 50bps | +8% (immediate) | Dollar weakens, risk appetite returns |

| Oct–Dec 2024 | Post-cut period | +73% | ETF flows + halving narrative + rate lag |

Notice January to June 2023 in that table. The Fed was still hiking rates — and Bitcoin went up 83%. The market had already decided that peak rates were near and started pricing in future rate cuts. This is the single biggest mistake retail investors make: reacting to what the Fed did rather than what the market expects the Fed to do next.

The Timing ParadoxWhen Fed hikes trigger liquidations, BTC often drops 15%+ in 48 hours as leveraged positions unwind. Understanding Bitcoin crash liquidity risk helps traders navigate margin call cascades that overshoot fundamentals by 20-30% before stabilizing.

How Long After a Fed Rate Cut Does Bitcoin Actually Rally?

The answer is: it depends on whether the cut was “good news” or “bad news.”

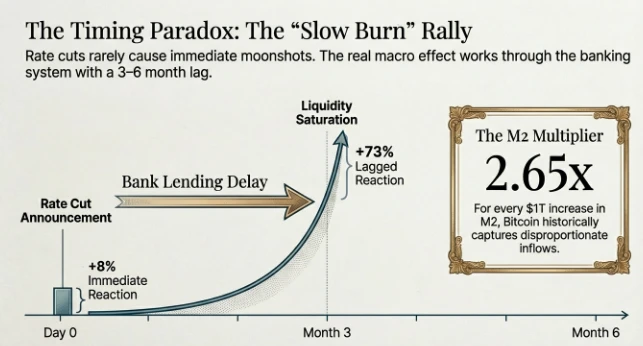

When the September 2024 Fed cut happened — the first cut after 14 months of holding rates at a 23-year high — Bitcoin jumped roughly 8% within 72 hours. Straightforward. Dollar weakened, risk appetite returned, speculative money flowed back in.

But the real gains came later. Three months after that cut, Bitcoin had risen approximately 73% from its pre-cut levels. The immediate 8% was the headline — the 73% was the actual macro effect working through the system with lag.

This lag happens because:

- M2 money supply takes months to expand after rate cuts as banks restart lending cycles.

- Institutional allocation decisions (rebalancing into risk assets) happen quarterly, not daily.

- Retail investor psychology needs to see sustained gains before FOMO kicks in and brings new capital.

- Bitcoin ETF flows (from 401(k) auto-investing) accumulate steadily over months, not in one burst.

2.65×Estimated M2 multiplier effect on Bitcoin — for every $1T increase in M2 money supply, Bitcoin has historically captured a disproportionate inflow relative to its market cap. This lag is what creates the “slow burn” rally after rate cuts.

Fed tightening contracts M2 money supply, forcing portfolio managers to dump high-beta assets like BTC. This central bank monetary policy transmission explains why Bitcoin leads equities in reacting to liquidity shifts despite having no cash flows.

Why Does Bitcoin Sometimes Crash Immediately After a Rate Cut? The Recession Signal Problem

This is the part that confuses almost everyone the first time they see it happen.

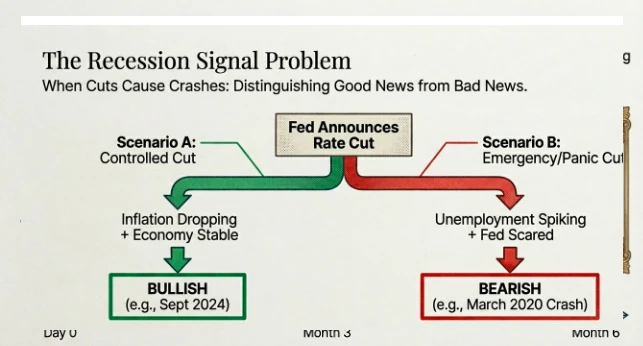

On March 15, 2020, the Federal Reserve announced an emergency rate cut of 100 basis points — one of the largest single-day cuts in history. Bitcoin dropped. Hard. Within hours.

How? The cut wasn’t a gift — it was a panic signal. The Fed cutting by 1% in an emergency session, before a scheduled meeting, told markets: something is seriously wrong. Investors rushed to cash, selling everything including Bitcoin.

Rate cuts are bullish for Bitcoin only when they signal “we’re easing policy to stimulate a healthy economy.” They’re bearish when they signal “we’re cutting because the economy is collapsing and we’re scared.”— The distinction that separates profitable macro traders from reactive retail investors

The practical difference: watch the Sahm Rule (a recession indicator based on unemployment rate changes) alongside Fed decisions. If the Sahm Rule is triggering at the same time as rate cuts, the cuts may be chasing a recession — not preventing one. In that scenario, Bitcoin typically sells off regardless of the cut.

The September 2024 cut was different — inflation was already declining, unemployment was stable, and the cut felt “controlled.” That’s why Bitcoin rallied rather than crashed.

Fed officials’ Friday remarks spark Sunday night sell-offs in 24/7 crypto markets. This explains why crypto crashes appear worse than warranted—25bps hikes justify 5% corrections rationally, but fear-driven thin liquidity produces 15% weekend drawdowns instead.

How Do Bitcoin ETFs Change the Interest Rate Sensitivity Equation?

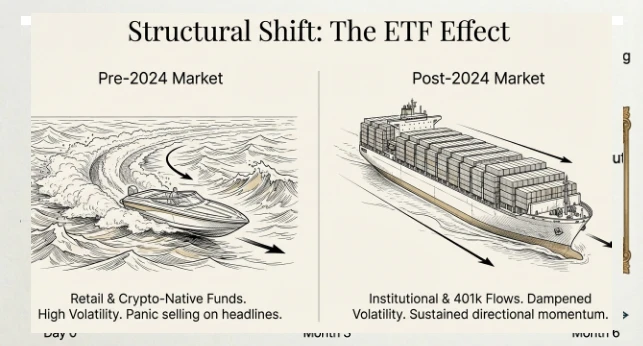

Before January 2024, when the first spot Bitcoin ETFs (like BlackRock’s IBIT and Fidelity’s FBTC) were approved in the United States, Bitcoin’s price was driven primarily by retail traders and crypto-native funds. That created extreme volatility — 20% swings in 48 hours were common around Fed meetings.

Post-ETF, something structurally changed. Institutional and retirement money began flowing in through 401(k) auto-investing programs and wealth management allocations. These buyers don’t watch FOMC press conferences and panic-sell. They buy on a schedule, regardless of what Jerome Powell said on a Tuesday afternoon.

By Q3 2025, Bitcoin ETFs had accumulated over $118 billion in total inflows. The implication: a meaningful portion of Bitcoin’s buy-side demand is now rate-insensitive. This doesn’t eliminate the correlation with rates — it dampens the immediate volatility while extending the directional move over a longer timeframe.

Think of it this way: before ETFs, Bitcoin reacted to rate hikes like a speedboat — rapid and violent turns. Post-ETF, it’s more like a cargo ship — it still turns in the same direction, just more slowly and with less sloshAlgorithmic trading reacts to CPI releases within milliseconds, clustering daily crypto declines around payrolls, FOMC minutes, and inflation reports. Smart traders hedge ahead of these predictable volatility spikes using options or stablecoin allocations.

Why Are Corporate Treasury Buyers Like MicroStrategy Insensitive to Fed Rate Changes?

MicroStrategy (now rebranded Strategy) has accumulated over 450,000 BTC at an average cost around $62,000 per coin as of early 2026. Their buying didn’t slow during the 2022 rate hike cycle. It accelerated.

The reason is behavioral, not financial. Corporate treasury buyers are operating on a 5–10 year horizon. They’re not looking at whether they can earn 5% in Treasuries instead. They’re making a structural bet that Bitcoin’s purchasing power will exceed the dollar’s over a decade. Fed rate cycles are quarterly phenomena — they’re thinking in decades.

This creates an interesting dynamic: even during rate hike cycles, there’s a class of buyer that does not care about the opportunity cost argument. They’re not choosing between Bitcoin and a 5.3% T-bill. They’re choosing between holding dollars (which they believe will lose value long-term) versus Bitcoin (which they believe will gain value long-term).

This group’s existence explains why Bitcoin’s 2022 drawdown stopped at $15,500 rather than going to zero — there were buyers who saw the 75% decline as a buying opportunity regardless of Fed policy.

Do Institutional Investors Treat Bitcoin Like a Tech Stock or Digital Gold During Rate Cycles?

In 2022, Bitcoin’s 90-day correlation with the NASDAQ 100 reached 0.92 — essentially moving in lockstep with tech stocks. Both assets got sold as rate hikes hit. The “digital gold” narrative collapsed as Bitcoin behaved like a high-beta technology bet, not a hedge.

In late 2024, something shifted. As geopolitical uncertainty increased (U.S.-China trade tensions, Middle East instability), Bitcoin’s correlation with NASDAQ fell to around 0.55 while its correlation with gold crept higher. Institutions began treating it differently — not identically to gold, but with more “store of value” characteristics than pure tech exposure.

The practical takeaway: Bitcoin’s narrative determines its correlation regime. During “everything up” or “everything down” macro environments, it acts like a risk asset (high NASDAQ correlation). During localized dollar-debasement fears or geopolitical crises, it acts more like gold (lower NASDAQ correlation, higher gold correlation). Rate hike impact depends heavily on which regime is currently activeAlgorithmic trading reacts to CPI releases within milliseconds, clustering daily crypto declines around payrolls, FOMC minutes, and inflation reports. Smart traders hedge ahead of these predictable volatility spikes using options or stablecoin allocations.

How Does the Dollar Index (DXY) Predict Bitcoin Moves Better Than Fed Rates Alone?

Here’s a genuinely useful finding that most retail crypto investors don’t know: the DXY (U.S. Dollar Index, which measures the dollar against a basket of major currencies) has a stronger and more consistent inverse correlation with Bitcoin than the Federal Funds Rate itself.

The DXY-Bitcoin correlation has historically ranged around -0.70 to -0.80 over rolling 6-month windows. The Fed Funds Rate correlation is weaker — around -0.30 to -0.45 over the same windows.

Why does this matter practically? Because the DXY moves before the Fed acts. Currency markets are forward-looking and often price in rate changes 2–4 weeks before the FOMC announcement. If you’re monitoring the DXY trend and it’s rising sharply, that’s often an early signal of Bitcoin headwinds — even before the Fed meeting happens.

A strengthening dollar (DXY moving from 100 to 108, as it did in 2022) means global capital is flowing into dollar assets. That’s the same capital that would otherwise go into risk assets like Bitcoin. A weakening dollar (DXY falling from 104 to 98, as in late 2024) is historically a reliable early indicator of Bitcoin strength.

Practical Tip

Watch the DXY before every FOMC meeting. If the dollar has already risen 3–5% in anticipation of a hike, most of Bitcoin’s downward pressure may already be priced in. If the dollar has risen only slightly and the hike surprises markets, expect a sharper immediate Bitcoin sell-off.

Why Did Bitcoin Crash in August 2024 Despite Fed Rate Cut Expectations? The BoJ Carry Trade Unwind

August 2024 was a masterclass in why you can’t look at the Fed in isolation. The Bank of Japan (BoJ) — Japan’s central bank — unexpectedly hiked its interest rates. This sounds completely unrelated to Bitcoin. It wasn’t.

Here’s what happened: for years, traders had been borrowing money in Japanese yen at near-zero interest rates (Japanese rates were essentially 0%) and converting it into dollars to buy higher-yielding assets — including Bitcoin. This is called a carry trade.

When the BoJ raised rates, that cheap yen borrowing suddenly got more expensive. Traders had to close their positions: sell Bitcoin (and other assets), buy yen, repay the loans. This triggered a cascade. Bitcoin fell roughly 26% in August 2024 even as the Fed was signaling coming rate cuts. The VIX (Wall Street’s fear gauge) spiked to 65 — the highest since COVID.

The lesson: global central bank policy, not just the Fed, moves Bitcoin. The BoJ, ECB, and Bank of England all influence global dollar liquidity and risk appetite. Monitoring only the Fed gives you an incomplete picture.

Why Do Retail Investors Sell Bitcoin Into Rate Hikes Despite Saying They’ll “Buy the Dip”?

Everyone has seen the meme: “I’ll buy more if it dips to $X.” And then it dips to $X and they don’t buy — they sell too.

Behavioral finance gives us the answer. There are two forces at work simultaneously during rate hike cycles:

Loss aversion: Humans feel the pain of losses roughly 2.5× more intensely than the pleasure of equivalent gains. When Bitcoin falls 20%, the psychological pain pushes people to “stop the bleeding” by selling, even when their rational mind told them to buy the dip. The magnitude of the loss overwhelms the pre-commitment.

Margin call cascades: Many retail investors hold Bitcoin on exchanges using leverage (borrowed funds to amplify their position). When Bitcoin drops 10–15%, their broker automatically liquidates their position to cover the borrowed amount. This forced selling creates the cascading crashes you see during rate hike cycles — not a single smooth decline, but sharp sudden drops followed by partial recoveries, then more drops.

During the March 2022 Fed rate hike cycle, Coinbase reported significant net exchange inflows (Bitcoin moving from wallets onto the exchange — a sign of intent to sell) in the 72 hours following each FOMC announcement. The on-chain data confirmed what behavioral finance predicted: retail panic-sold at the announcement.

How Do Crypto Whales Actually Position Before FOMC Meetings?

On-chain data from blockchain analytics platforms like Glassnode reveals a consistent pattern in the 48–72 hours before major Fed decisions: exchange outflows increase significantly among large wallet addresses (wallets holding 1,000+ BTC, commonly called “whales”).

Exchange outflows mean Bitcoin is moving from exchanges to private wallets. That’s a sign of accumulation intent — buying and moving to cold storage rather than leaving on an exchange for quick selling.

This creates a counterintuitive pre-FOMC dynamic: the people with the most capital are often accumulating while retail participants are reducing exposure. Then the announcement happens. If it’s a surprise hike or hawkish language, retail panic-sells — often into whale bids. If it’s in line with expectations, prices stabilize. If it’s a dovish surprise, the accumulated positions become instantly profitable.

This doesn’t mean whales always get it right. But the pattern of on-chain accumulation before uncertainty events, followed by retail selling into that uncertainty, repeats frequently enough to be worth monitoring.

Section 6 · The Contrarian Scenarios

When Should You Actually Worry About Rate Cuts Causing Bitcoin to Drop?

The rate cut scenarios that hurt Bitcoin are the ones that signal something went wrong in the economy.

| Cut Type | Signal | Expected BTC Reaction | Historical Example |

|---|---|---|---|

| Controlled cut (25bps, scheduled) | Economy softening, inflation under control | Bullish (delayed) | Sept 2024 — +73% over 3 months |

| Emergency cut (50–100bps, unscheduled) | Something is seriously wrong | Bearish (immediate) | March 2020 — sharp initial drop |

| Recession cuts (multiple, rapid) | Unemployment rising, credit crunch | Bearish (sustained) | 2008 cuts — broad asset decline |

| Pivot signal (first cut after long hike cycle) | Peak tightening passed | Strongly bullish (over months) | 2024 pivot cycle |

Could Bitcoin Actually Benefit From a Stagflation Scenario Where Rates Stay High But Inflation Persists?

This is the contrarian scenario worth understanding, even if it’s uncomfortable for Bitcoin bears to consider.

Stagflation is when you have high inflation and stagnant economic growth simultaneously. It’s the worst-case scenario for traditional policymakers because raising rates slows growth further, while not raising rates allows inflation to run. The 1970s are the historical reference point.

In that environment, real interest rates (nominal rate minus inflation) can actually be negative — meaning your 4% Treasury bond is losing 2% of purchasing power annually if inflation is 6%. In that scenario, the “opportunity cost” argument for Bitcoin weakens. A 4% nominal return that loses to 6% inflation isn’t a compelling alternative to Bitcoin, which — despite volatility — has outpaced inflation over any 4+ year holding period since 2015.

We’re not currently in stagflation (as of early 2026), but the 2025 tariff environment created meaningful goods inflation concerns that are worth monitoring. If inflation reaccelerates while the Fed is reluctant to hike further (due to debt load and political pressure), the “digital gold” narrative could reassert itself strongly — even with rates elevated.

How Should You Think About Your Bitcoin Position Around Fed Decisions?

This is not trading advice. But here’s how to think about it clearly, without the gambling mentality that destroys most retail portfolios.

✓ What to Do

- Monitor the DXY trend 2–4 weeks before FOMC — it often leads Bitcoin’s direction

- Reduce leverage before Fed meetings (unexpected outcomes happen more than people expect)

- Focus on the surprise element of the decision, not the decision itself

- Watch whether cuts accompany rising or falling unemployment — context is everything

- Think in 6–12 month windows for macro effects, not days

✗ What Not to Do

- Don’t make large Bitcoin trades on the day of the FOMC announcement

- Don’t use leverage around Fed week — volatility expands 200–300% around announcements

- Don’t confuse “rates fell” with “Bitcoin will immediately rise” — timing matters

- Don’t ignore other central banks (BoJ, ECB) — they move global liquidity too

- Don’t sell based on rate hike headlines alone if the cut/hike was already priced in

Pre-FOMC Checklist: A Week Before Each Fed Decision

- 7 days out: Check current DXY level and 4-week trend direction. Rising DXY = headwind for Bitcoin.

- 5 days out: Review fed funds futures (CME FedWatch Tool) — see what the market already expects. If 95% probability of a 25bps hike is priced in, most of the move has already happened.

- 3 days out: Reduce or close leveraged Bitcoin positions. The announcement can move Bitcoin 8–15% in either direction in minutes.

- 2 days out: Monitor on-chain exchange flows. Outflows (Bitcoin leaving exchanges) suggest accumulation by larger holders.

- Decision day: Don’t trade immediately on announcement. Wait 2–4 hours for the initial volatility to settle and the real direction to emerge.

- Post-decision: Reassess macro picture with new information — not what the rate change means for today, but what it signals for the next 3–6 months of monetary policy direction.

The FOMC announcement is the noisiest possible moment to make a Bitcoin decision. The signal is in the trend that comes after — not the spike or crash on announcement day.

Quick Answers to Common Follow-Up Questions

Does Bitcoin always drop when the Fed raises rates?

No. The relationship holds over long cycles but breaks frequently in the short term. Bitcoin rose 83% from January to June 2023 while the Fed was still hiking — because markets had already priced in peak rates. The correlation is real but imperfect.

What’s the biggest factor: rate hikes or rate cuts?

Rate hike cycles cause larger average declines than rate cut cycles cause rallies. The 2022 cycle wiped out 75% of Bitcoin’s value. The 2024 cut cycle produced around 73% gains. But the hike-driven decline was faster and more severe — hikes tend to hurt more than cuts help, primarily because of forced deleveraging cascades.

Is Bitcoin a hedge against inflation or a risk asset?

Currently both, depending on the timeframe. Over 4+ year periods, Bitcoin has consistently outpaced inflation. Over quarterly periods, it often moves with tech stocks. The narrative shifts based on macro environment — during rate hike cycles, it acts like a risk asset. During dollar debasement concerns, it acts more like gold.

Do Bitcoin ETFs change how it reacts to rate moves?

Yes. ETF inflows create a structural bid from institutional and retirement money that is less rate-sensitive than retail speculation. This has reduced immediate volatility around Fed meetings but hasn’t eliminated the directional relationship. The moves are now slower and more sustained rather than violent and short-lived.

Should I buy Bitcoin before or after a Fed rate cut?

This is not financial advice. Historically, the best macro entry points for Bitcoin have been when the market begins pricing in rate cuts — 3 to 6 months before the first actual cut — not after. By announcement day, a significant portion of the expected move has already happened. After the first cut, the 3–6 month lag for M2 expansion to fully materialize is what drives the sustained rally.

How reliable is the Bitcoin-interest rate relationship for predicting prices?

It’s one useful factor among many, not a standalone predictor. Historical backtesting suggests that “Fed is hiking → avoid Bitcoin leverage” has a roughly 68–72% accuracy rate as a directional signal. But the magnitude of moves varies enormously, and regime changes (like the ETF approval in January 2024) can break historical patterns. Use it as one lens, not the only lens.

Final Thought

The One Thing That Actually Matters

After going through all of this — the four transmission channels, the timing paradox, the ETF mechanics, the BoJ carry trade, the behavioral patterns — there’s one thing that ties it all together:

Bitcoin doesn’t react to interest rates. It reacts to global dollar liquidity. Interest rates are just one lever that controls that liquidity. The Fed Funds Rate, the DXY, M2 money supply, the BoJ’s rate decisions, and the ECB’s policy direction are all part of the same interconnected system of dollar availability around the world.

When dollar liquidity is abundant and cheap, speculative capital flows more freely into high-risk, high-reward assets — including Bitcoin. When it’s scarce and expensive, that capital retreats to safety.

The clearest leading indicator of that liquidity, in real time, is the DXY. Watch the dollar. Then you’ll understand Bitcoin’s macro environment — not perfectly, and not in real time, but with enough lead time to avoid the worst reactive mistakes.

Everything else — the FOMC press conferences, the dot plots, the “surprise” hikes — are just the mechanisms through which global dollar liquidity changes. The mechanism matters less than the direction of the outcome.

Educational Disclaimer: This article is for informational and educational purposes only. Nothing written here constitutes financial advice, investment advice, or a recommendation to buy, sell, or hold any cryptocurrency or financial instrument. Cryptocurrency markets are highly volatile and speculative. Past correlations between interest rates and Bitcoin prices do not guarantee future outcomes. Always consult a qualified financial advisor before making investment decisions. The author holds no responsibility for decisions made based on this content.